Unincorporated Nonprofit Association Education

Private Association. Clear Governance. Enduring Mission.

A UNA is a group organized around a shared nonprofit purpose, without necessarily forming a corporation. Its strength comes from purpose, articles, membership rules, records, and ongoing conduct — not the name alone.

Recognition, property rights, liability treatment, tax status, and reporting obligations vary by state, facts, governing documents, and administration. Qualified legal and tax review is required.

The Foundation

What a UNA Is and Is Not

A UNA is generally a membership-based association created by agreement for a nonprofit purpose. Depending on state law, it may hold property, enter contracts, maintain records, and continue beyond changes in membership.

Just as important — a UNA is not automatically:

- A 501(c)(3), or tax exempt

- Anonymous, or immune from lawsuits

- Exempt from reporting, or outside state or federal law

- A substitute for legal or tax advice

The governing documents and the actual operation are what matter.

The Visual Language

The UNA Is the Vault

The UNA is represented as a vault because the structure depends on disciplined internal order — membership, mission, articles, officer authority, controlled records, and property stewardship kept inside.

Inside the Chamber

The Core Components

Mission

A clear nonprofit purpose, followed consistently — not just written down.

Members

- Admission and voting rights

- Resignation or removal

Articles of Association

- Name, purpose, membership framework

- Officer roles and decision authority

Officers & Authorized Representatives

- Who may sign contracts or manage accounts

- Who maintains records

Records

- Articles, amendments, membership registry

- Banking, tax, and compliance files

Property Stewardship

Documented, titled, insured, and administered per the governing documents.

The Standard

The Structure Must Operate Like a Real Association — and Outlast Any One Person

A UNA isn't a document package that creates automatic benefits. Its credibility comes from conduct; its continuity comes from rules and records, not slogans. A structured review asks:

- Is the nonprofit purpose real and consistently followed?

- Are members and officers clearly identified, with decisions documented?

- Are finances separated, recorded, and contracts signed by authorized people?

- Are successor officers and replacement procedures defined?

- Are dissolution or continuation decisions addressed in the articles?

Relevance doesn't mean fit — each situation requires state-specific and professional review.

The Honest Conversation

Tax, Reporting & Professional Review

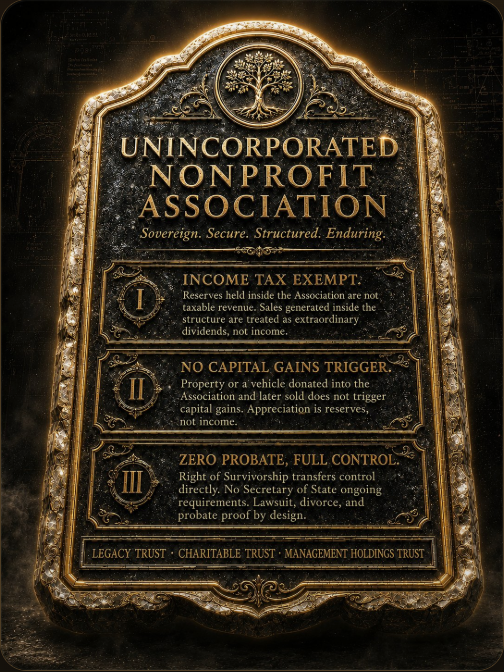

A UNA is not automatically exempt from federal or state income tax merely because it is nonprofit in purpose. Treatment depends on organizational purpose, activities, governing documents, income sources, and federal and state requirements.

- State registration or licensing requirements

- Adequate insurance and liability coverage

- Filing deadlines and recurring compliance obligations

- Qualified legal and tax review before and after formation

The Next Step